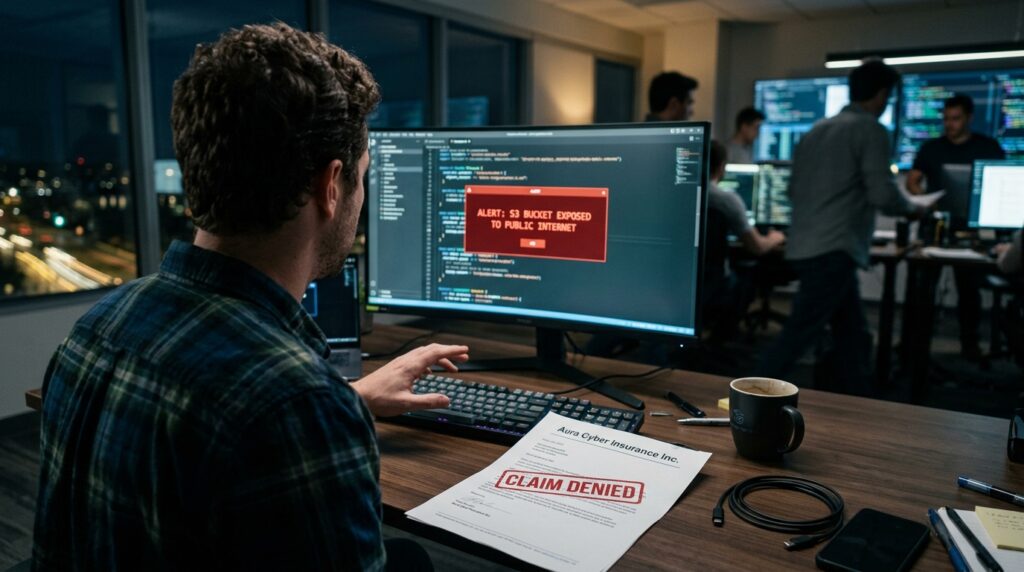

Two years ago, I watched a colleague’s SaaS platform bleed out fifty thousand user records in less than twenty minutes. It wasn’t a sophisticated, cinematic state-sponsored cyberattack. It was a single, overlooked line in an automated Terraform script that left an AWS S3 bucket exposed to the public internet during a midnight deployment.

The team didn’t panic initially. Why would they? They had a premium $2 million cyber liability insurance policy. They filed the claim by sunrise, fully expecting the insurance carrier to step in, clean up the mess, handle the compliance notifications, and cover the legal fallout.

Three weeks later, the denial letter arrived.

The insurance company didn’t just deny parts of the claim; they completely walked away. They cited a specific, buried clause regarding “failure to maintain reasonable security standards” and “intentional automation modifications.”

That was my wake-up call. If you are running cloud infrastructure today and relying on standard, off-the-shelf cyber insurance to save you when an automated pipeline goes sideways, you are likely uninsured. Here is exactly why carriers are rejecting these automated cloud breach claims, and what you need to change in your setup before the worst happens.

The Illusion of the “All-Risk” Cyber Policy

When you buy a standard cyber insurance policy, the broker usually gives you a sleek PDF promising coverage for data breaches, ransomware extortion, and business interruption. It sounds great on paper. But insurance companies are in the business of assessing risk based on predictable models.

The traditional insurance model assumes a static network: you have a firewall, you have some servers, you update your antivirus every Tuesday, and you use a VPN.

Cloud environments don’t work that way. In modern cloud setups, your infrastructure is defined as code (IaC). A developer modifications a file, pushes it to GitHub, an automated CI/CD pipeline triggers, and within seconds, your entire network topology changes. This dynamic shifting completely breaks the underwriting logic of traditional cyber policies.

When a breach happens because an automated system spun up a vulnerable resource, the insurance company’s forensic team won’t look at what your security policy says. They look at what your automated code did.

Why Automation Triggers the Dreaded “Exclusion Clause”

If you read the fine print of your policy, you will find a section dedicated to exclusions. Lately, claims adjusters are using three specific arguments to deny cloud automation breaches:

1. The “Administrative Oversight” vs. “System Failure” Distinction

Most policies cover data breaches caused by unauthorized third-party hacks or sudden system failures. However, if your automated deployment script explicitly sets a database security group to 0.0.0.0/0 (open to the world), the insurer argues this isn’t a hack or a system failure. It is an administrative configuration error. To them, you essentially unlocked your front door, threw away the key, and invited the world inside.

2. Failure to Follow “Minimum Required Security Standards”

When you apply for cyber insurance, you fill out a lengthy questionnaire. You check boxes saying you use multi-factor authentication (MFA), regular vulnerability scanning, and strict access controls.

But what happens when an automated Jenkins or GitLab runner bypasses MFA to execute a deployment, and that runner gets compromised? The insurer will argue that by hardcoding API keys or credentials into an automated script to bypass manual security checks, you violated the core risk profile you agreed to maintain.

3. The Definition of “Insured Property”

Many older or lower-tier policies still define the insured perimeter by physical assets or dedicated private networks. If a malicious script creates an unauthorized, rogue AWS account under your organization billing via an unthrottled API, the insurance company might claim that specific dynamic infrastructure wasn’t a registered asset under the original policy terms.

A Real-World Scenario: The API Loop That Cost a Fortune

Let’s look at how this happens in plain English, without the confusing technical jargon.

Imagine a growing fintech app that uses third-party APIs to process micro-transactions. To speed up development, the engineering team sets up an automated scaling script. If server traffic spikes, the script automatically provisions new virtual machines via Microsoft Azure to handle the load.

One night, an attacker finds an unsecured API endpoint and floods it with automated requests. The scaling script does exactly what it was programmed to do: it rapidly provisions hundreds of new cloud instances to keep up with the artificial traffic.

The attacker uses these freshly minted, automated instances to mine cryptocurrency and scrape neighboring databases. By the time the team notices the anomaly at 8:00 AM, the company has accumulated a $150,000 cloud infrastructure bill, alongside a massive data exposure.

The insurance company rejects the claim for two reasons:

- The data exposure happened on temporary, automated instances that did not exist when the policy was audited.

- The financial loss from the massive cloud bill was generated by the company’s own automated system, not directly by the hacker’s hands.

Mistakes Most Dev Teams Make with Insurance Alignment

Through auditing setups after the fact, I see the same three mistakes happening across almost every software and tech team:

- Leaving the Insurance Policy with Legal: The engineering and DevOps teams rarely see the actual cyber insurance policy. The executive team signs it, legal files it, and the engineers keep deploying code completely blind to the compliance requirements dictated by the underwriter.

- Treating Infrastructure as Code (IaC) Separately from Security: Teams focus heavily on making sure automated deployments are fast and functional, but they don’t integrate static code analysis into the pipeline to check for security misconfigurations before the code goes live.

- Assuming Managed Services Cover Everything: There is a dangerous belief that if you use AWS, Google Cloud, or Azure, security is entirely their problem. Cloud providers operate on a shared responsibility model. They secure the cloud hardware; you secure the configuration inside it. If your automation breaks your configuration, that is on you.

How to Fix Your Infrastructure to Guarantee Claim Approval

You don’t have to stop using automation. You just need to make your automation provably secure so that an insurance adjuster cannot find a loophole to deny your claim. Here is a step-by-step approach to protecting your business:

Step 1: Implement “Policy as Code” (PaC)

Before any automated script can modify your live cloud environment, it must pass a security gate. Use tools like Open Policy Agent (OPA), Checkov, or tfsec inside your CI/CD pipelines. These tools automatically scan your Terraform, CloudFormation, or Ansible scripts for misconfigurations (like open ports or unencrypted databases) before they deploy. If a script fails the security check, the pipeline breaks, and nothing goes live. This creates a clear, auditable trail showing you took every reasonable step to prevent errors.

Step 2: Use Ephemeral Credentials

Never, under any circumstances, hardcode long-lived API keys or access tokens into your automation scripts or GitHub repositories. If an attacker gains access to your repository, they gain control of your cloud. Use tools like HashiCorp Vault or cloud-native solutions like AWS Secrets Manager to generate short-lived, temporary credentials that expire after a few minutes.

Step 3: Enforce Immutable Infrastructure

Stop logging into cloud consoles manually to fix things. If something breaks or needs an update, destroy the old instance and deploy a brand-new one via your verified pipeline. This prevents “configuration drift,” where small, manual changes over time make your actual cloud security profile look completely different from the clean environment you showed your insurance broker.

Step 4: Bridges the Gap Between DevOps and Your Insurance Broker

Take your lead DevOps engineer to the next insurance renewal meeting. Have them explicitly explain your CI/CD pipelines, deployment strategies, and how you use automation to the broker. Demand a policy rider or endorsement that explicitly covers “failures, data breaches, or third-party liabilities arising from automated deployments, infrastructure-as-code executions, and programmatic cloud scaling.” If the broker looks confused, find a specialized tech insurance broker who understands cloud architecture.

Final Thoughts

Automation is the only way to scale a modern business, but it moves faster than the legal systems meant to protect us. Insurance companies are businesses looking to minimize their losses. If your automated systems are deploying unverified, unchecked configurations into production, you are essentially hand-delivering an escape hatch to your insurance provider.

Take an hour this week to look at your deployment pipelines, download your current cyber insurance policy, and look for the gaps. Finding out your automation isn’t covered during a live breach is a multi-million-dollar mistake you don’t want to make.