Last year, I sat in a logistics terminal in Kentucky watching a fleet manager stare blankly at an empty loading dock. A high-value shipment of consumer electronics—worth just over $340,000—had been picked up eighteen hours earlier. The tracking link provided by the broker was dead. The broker’s phone number was disconnected. The carrier listed on the rate confirmation sheet had never heard of the load.

The cargo didn’t just go missing; it vanished into thin air.

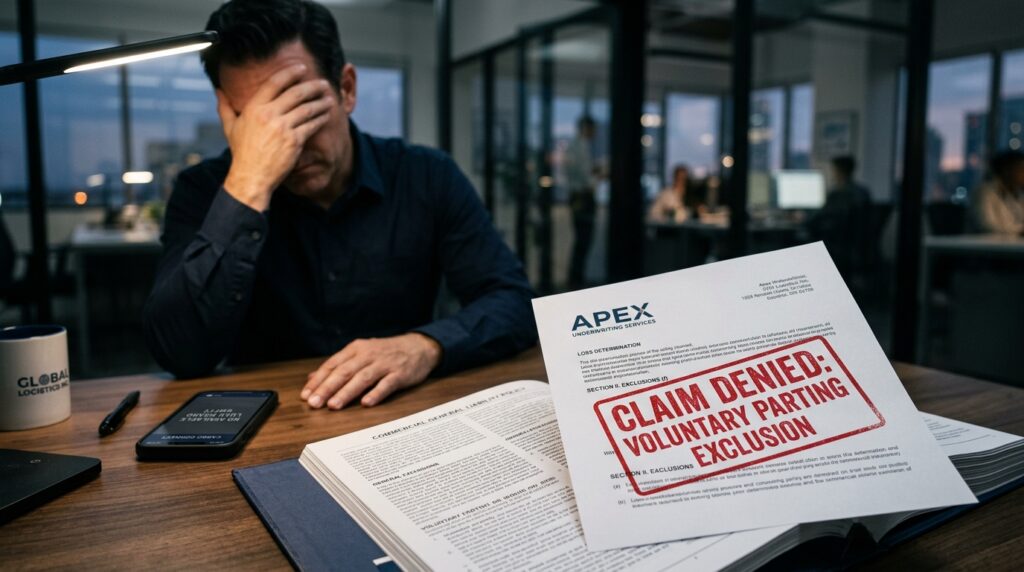

Like any responsible logistics operation, the team immediately gathered the paperwork, pulled up their Inland Marine insurance policy, and filed a claim for cargo theft. They assumed they were protected. They had paid their premiums on time, double-checked the carrier’s safety ratings on the FMCSA portal, and followed basic compliance.

Then came the hammer blow from the underwriter. The claim was denied.

The insurance company didn’t deny it because the cargo wasn’t stolen. They denied it because of how it was stolen. The policy covered physical theft, hijacking, and accidental damage. It did not, however, cover “Voluntary Parting”—a tiny, devastating loophole that phantom freight brokers use to rob logistics companies blind while ensuring the insurance company never has to pay a single dime.

If you are running a brokerage, a dispatch service, or a fleet management operation today, you need to understand exactly how this modern identity theft works and why your current standard cargo policy might leave you completely exposed.

What is a Phantom Broker?

To understand why insurance companies run away from these claims, you have to understand the modern identity mechanics of a phantom broker setup.

Years ago, cargo theft meant someone cutting a padlock on a trailer at a truck stop. Today, it’s entirely digital. A phantom broker is a fraudster who steals the corporate identity of a legitimate, licensed freight brokerage or motor carrier. They set up fake accounts on digital load boards like DAT One or Truckstop using spoofed phone numbers, lookalike email domains (e.g., changing an example-logistics.com to examplelogistics-inc.com), and forged certificates of insurance.

Once they get inside the system, they bid on high-paying loads. When they win the load from a shipper, they turn around and re-broker it to an actual, unsuspecting truck driver. The real driver picks up the freight, thinking they are working for a legitimate broker.

Halfway through the route, the phantom broker contacts the driver with “updated delivery instructions,” redirecting the truck straight to a fraudulent cross-dock or a blind warehouse. The driver unloads the freight, gets paid a small fuel advance by the scammer, and drives away. By the time the original shipper realizes the freight never arrived at the true destination, the phantom broker has deleted the accounts, cashed out the load payout, and disappeared.

The Voluntary Parting Loophole Explained

When you file an Inland Marine or motor truck cargo claim for this type of event, the adjuster immediately pulls up the exclusions page of your policy. They are looking for one specific phrase: Voluntary Parting due to Fraud, Trick, or Device.

Here is the cold, hard logic the insurance company uses to reject your claim:

The policy is designed to cover fortuities—things that happen completely against your will, like an armed robbery or a trailer being broken into at night. But in a phantom broker scenario, you signed the rate confirmation. You handed the bills of lading to the driver. You or your warehouse staff willingly loaded the pallets onto the trailer.

Because you handed over the goods voluntarily—even though you were completely tricked by a fake identity—the law views it as a scam, a corporate fraud, or a bad business transaction rather than a classic physical theft.

Unless your policy explicitly features a specific endorsement that overrides this exclusion, your standard Inland Marine coverage is practically useless against digital fraud.

Mistakes Most Logistics Teams Make During Carrier Vetting

When we audited the onboarding processes of companies that fell victim to these ghost networks, we noticed the same three critical procedural gaps:

- Relying Solely on Static PDF Documents: Scammers are incredibly skilled with Adobe Acrobat. They can modify an insurance certificate or an MC authority letter in less than five minutes, swapping out names, phone numbers, and expiration dates. If your team is just accepting emailed PDFs without verifying them at the source, you are gambling with your freight.

- Trusting the Phone Number on the Load Board: When a broker or carrier calls from a load board listing, dispatchers often call them back on the number provided in the email signature or the bid comment section. Scammers use burner apps and VOIP routes to make these numbers look local or legitimate.

- Ignoring the “Age” of the Digital Footprint: Teams often check if an MC number is active, but they fail to look at how recently the contact information, email server, or domain name was registered. A broker entity that has been around for ten years but suddenly changed its contact email to a Gmail address three days ago is a massive red flag.

Step-by-Step Security Strategy to Close the Loophole

You do not have to stop using digital load boards, but you do need to completely change how your operation verifies identity and handles policy structuring. Here is exactly how to secure your workflow:

Step 1: Force Direct Verification (The Call-Back Method)

Never use the phone number or email address provided inside an incoming email pitch or a rate confirmation sheet. Instead, copy the MC (Motor Carrier) or USDOT number of the entity you are dealing with. Go directly to the official FMCSA Licensing and Insurance (L&I) website or use a trusted platform like Carrier411. Pull the registered phone number listed on their official federal registration and call that number directly to confirm the person bidding on your load actually works for that specific company.

Step 2: Analyze Email Headers and Domain Age

If you receive an email from dispatch@reliable-freight.com, don’t just glance at it. Run the domain through a free Whois lookup utility. If the actual freight company has been in business since 2012, but the domain reliable-freight.com was registered in a foreign country just forty-eight hours ago, you are dealing with a phantom entity spoofing a real brand.

Step 3: Implement Multi-Factor Location Checks

Before allowing a driver to leave the loading dock with high-value assets, require a digital check-in using automated visibility tools like Project44, FourKites, or a quick macro-compliance mobile ping. Verify that the physical tractor and trailer license plates match the paperwork exactly. If the driver claims they had to switch trucks at the last minute and the plates don’t match your system sheets, do not load the truck.

Step 4: Demand a “Deceptive Practices” Insurance Endorsement

Call your insurance broker immediately. Do not ask them if you are covered for “theft.” Ask them this exact question: “Does our policy contain an exclusion for Voluntary Parting, and do we have a Deceptive Practices or Fraudulent Pickup endorsement?” A true Deceptive Practices endorsement explicitly states that the policy will pay out if you voluntarily hand over cargo to someone who is intentionally misrepresenting their identity. If your broker cannot provide this endorsement, you need to find an underwriter who specializes in modern supply chain cyber-fraud risks.

Common Red Flags to Watch for on the Load Board

Train your dispatchers and logistics coordinators to spot these behavioral anomalies during negotiations:

| Red Flag Indicator | What It Usually Means |

| Below-Market Rate Demands | If a carrier or broker is willing to haul a difficult route for an absurdly low price, or conversely, if they offer to pay an inflated rate without negotiating accessorials, they are likely just trying to secure the cargo at all costs. |

| High Urgency / Anti-Verification Tactics | When a representative pressures your team to bypass normal onboarding steps because “the truck is outside right now” or “the driver is about to leave the area,” it is an intentional tactic designed to make you skip verification. |

| Generic Free Email Accounts | Legitimate freight brokerages spend money on corporate infrastructure. If a contact person tells you their corporate server is down and asks you to send paperwork to a Yahoo, Gmail, or ProtonMail account, halt the transaction. |

Final Thoughts

The logistics industry has evolved faster than standard commercial insurance policies. The threat is no longer just a physical lockpicker at a dark rest stop; it is an organized, digital enterprise operating behind clean screens halfway across the world.

If you are still operating on a traditional Inland Marine policy framework without verifying how your business handles digital identity verification, you are carrying an unhedged multi-million-dollar risk. Take the time to update your vetting tools, train your dispatch team on the call-back method, and get your insurance endorsement updated before a ghost broker claims your next shipment.